In any organisation where company buys and sells the goods on credit, at that organisation, we need to divide journal into subsidiary books.

One of these subsidiary books is purchase book. In purchase book, we record all transactions relating to credit purchases of goods only and these goods are trading goods.

Company deals in these goods and products. In this book, accountant does not record cash purchases and purchase of assets in which company does not deal.

Suppose shop of furniture's product is furniture and its credit purchase will be recorded in purchase book.

Its other name is bought book, purchase journal and purchase day book.

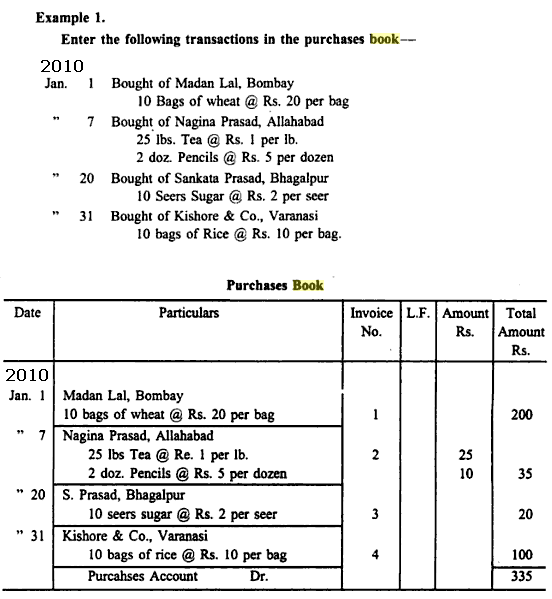

This book is maintained on the basis of invoice.

Accountant records quantity of products, rate and amount from invoice. Each transaction is recorded by giving invoice no.

One of these subsidiary books is purchase book. In purchase book, we record all transactions relating to credit purchases of goods only and these goods are trading goods.

Company deals in these goods and products. In this book, accountant does not record cash purchases and purchase of assets in which company does not deal.

Suppose shop of furniture's product is furniture and its credit purchase will be recorded in purchase book.

Its other name is bought book, purchase journal and purchase day book.

This book is maintained on the basis of invoice.

Accountant records quantity of products, rate and amount from invoice. Each transaction is recorded by giving invoice no.

Posting of Purchase Book

To fulfill double entry system, purchase book will be posted two accounts.

One account will be purchase account and other account will be creditor's account.

In purchase account, we will write total of purchases on credit basis.

We also open the creditors accounts by writing the name of creditor.

Suppose, we have purchased goods on credit from madan lal.

In madan lal account's credit side, we will write by purchases and will show Rs. 200.

Like this, we open all creditor's account.

Advantages of Purchase Book

- With this book, we can find, how much goods have been bought by us?

- It also tells us, how much many has to whom?

- This book is also helpful to make final accounts.

PURCHASE RETURN BOOK

Like other parts of subsidiary books, purchase return book is also part of sub-division of journal.

In this book, we record all goods which has return to our supplier because

In this book, we record all goods which has return to our supplier because

a) His goods are not according to our sample.

b) His stock was defective.

c) Goods were not sent according to our purchase order.

This book will reduce our payable amount to our creditors. This book's other name is return outwards book.

This book is written on the basis of debit note. Debit note is proof that we have returned the goods and creditor's account will be debited for reducing our payable amount to him.

Example:

Bike LTD purchases a mountain bike from BMX LTD for $100 on credit. Bike LTD later returns the bike to BMX LTD due to a serious defect in the design of the bike.

The initial purchase will be recorded as follows:

| $ | $ | ||

| Debit | Purchases | 100 | |

| Credit | BMX LTD | 100 | |

Upon the return of bike, the following double entry will be passed:

| $ | $ | ||

| Debit | BMX LTD | 100 | |

| Credit | Purchases Return | 100 | |

No further entry will be required as the payable due to BMX LTD has been reversed.

Purchase Returns - Cash Purchase

In case of cash purchases, the following double entry must be made upon sales returns:

| Debit | Receivable (increase in asset) |

| Credit | Purchases Return (decrease in expense) |

Example:

Bike LTD purchases a mountain bike from BMX LTD for $100 on cash. Bike LTD later returns the bike to BMX LTD due to a serious defect in the design of the bike.

The initial purchase will be recorded as follows:

| $ | $ | ||

| Debit | Purchases | 100 | |

| Credit | Cash | 100 | |

Upon the return of bike, the following double entry will be passed:

| $ | $ | ||

| Debit | BMX LTD (Receivable) | 100 | |

| Credit | Purchases Return | 100 | |

When BMX LTD will pay $100 owed to Bike LTD in respect of the purchases return, the following double entry will be recorded in Bike LTD's books:

| $ | $ | ||

| Debit | Cash | 100 | |

| Credit | BMX LTD (Receivable) | 100 | |

No comments:

Post a Comment